3.6 Strategy: Market Making

Key Takeaways

- Market making is providing liquidity on both sides of a market — buying from sellers, selling to buyers — and earning the spread

- Unlike directional trading, market making profits from volume and spread, not from predicting outcomes

- The primary risk is adverse selection — informed traders pick off your orders because they know something you don’t, leaving you with losing positions

- Market making in prediction markets requires $5,000+ in capital at the learning stage and scales to $100,000+ for professional operations

- This is not a beginner strategy — it requires order management skills, capital, and ideally API access for automation

Scope: This module explains how market making works in prediction markets, when it’s profitable, and what risks it carries. It provides the conceptual framework — not implementation code. For API-level execution, see the developer resources in Module 4.1: Building Your Trading System. This module applies the structural edge framework from Module 3.1.

What Market Makers Do

Every trade requires two participants: a buyer and a seller. But what happens when a buyer wants to buy and there’s no seller available? Or when a seller wants to sell and there’s no buyer?

Market makers solve this problem. They stand ready to buy AND sell at all times, providing liquidity to the market. In return, they earn the spread — the gap between their buy price and their sell price.

The Basic Mechanism

A market maker places two orders simultaneously:

- A bid (buy order) at a price below the current mid-price

- An ask (sell order) at a price above the current mid-price

If both orders fill, the market maker earns the difference regardless of the outcome.

Example:

Market: “Will the Fed hold rates in June 2026?” — current mid-price: $0.60

The market maker places:

- Bid: Buy “Yes” at $0.58 (100 contracts)

- Ask: Sell “Yes” at $0.62 (100 contracts)

If both sides fill:

- Bought 100 at $0.58 = spent $58

- Sold 100 at $0.62 = received $62

- Profit: $4.00 (the $0.04 spread × 100 contracts)

This profit is earned regardless of whether the Fed holds or cuts — because the market maker has equal and opposite positions that cancel each other out.

Why This Works

- Natural flow generates fills. Regular traders want to buy or sell for directional reasons. The market maker provides the other side of their trades

- The spread compensates for risk. The wider the spread the market maker quotes, the more they earn per fill — but a wider spread also means fewer fills because traders choose competitors with tighter quotes

- Volume scales the returns. A $0.04 spread on 100 contracts earns $4. The same spread on 10,000 contracts earns $400. Market making is a volume business

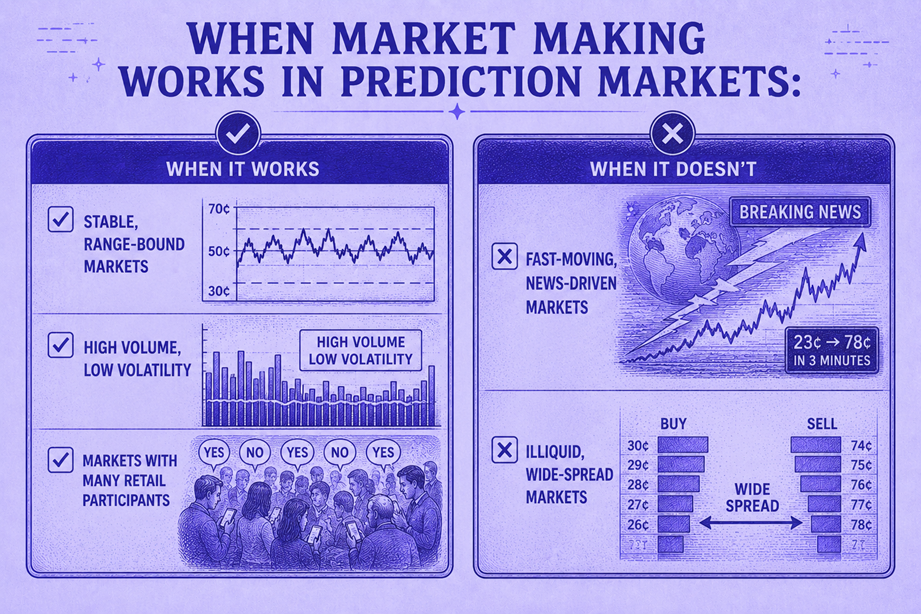

When Market Making Works in Prediction Markets

Not all prediction markets are suitable for market making. The ideal conditions are:

✅ Stable, Range-Bound Markets

Markets where the probability isn’t moving much — e.g., a far-off election that’s trading between $0.45 and $0.55 with no major news catalysts. The price oscillates within a range, and your bid and ask both fill repeatedly as the price bounces.

✅ High Volume, Low Volatility

More traders = more fills. Low volatility = the price doesn’t run away from your quotes. This is the goldilocks zone for market making.

✅ Markets with Many Retail Participants

Retail traders tend to use market orders (paying the spread), which is exactly what market makers want. Professional traders use limit orders (competing for the spread), which is what market makers don’t want.

❌ Fast-Moving, News-Driven Markets

When a major news event hits, the price moves rapidly. Your standing orders get filled on the wrong side: information traders buy your cheap asks because they know the price is about to rise, or sell into your high bids because they know the price is about to fall. You end up with a directionally exposed position at the worst possible time.

❌ Illiquid, Wide-Spread Markets

If the spread is already wide ($0.10+), the market likely has structural reasons for low liquidity — uncertainty about resolution, niche topic, or very long time to expiration. Providing liquidity in these conditions carries elevated risk.

Adverse Selection: The Primary Risk

Adverse selection is the market maker’s greatest enemy. It occurs when an informed trader — someone who knows the price is about to move — takes your order before you can cancel it.

How It Works

- You’re market-making on a Fed rate market. You have a bid at $0.58 and an ask at $0.62

- The BLS releases an unexpected inflation number at 8:30 AM. The “true” probability of a rate hold drops from 60% to 40%

- An informed trader instantly sells into your bid at $0.58, while the fair value is now ~$0.40

- You now own 100 “Yes” contracts at $0.58 that are worth ~$0.40. You’ve lost $18 per 100 contracts — far more than your $4 spread profit

The math is brutal: One adverse selection event can wipe out dozens of successful spread captures. This is why market making requires:

- Speed — the faster you can cancel your orders after news, the less adverse selection you experience

- Risk management — position limits and automatic hedging to contain losses

- Market selection — avoiding markets with upcoming news catalysts

Managing Adverse Selection

| Technique | How It Works | Who Uses It |

|---|---|---|

| Wide spreads before known events | Widen your bid-ask spread 5–10x before scheduled data releases, speeches, or votes. This creates a buffer against sudden moves | All market makers |

| Order cancellation speed | Use API access to cancel orders within milliseconds of detecting a price move. The faster you cancel, the less exposure | Semi-automated and professional |

| Position limits | Cap the maximum number of contracts on any single side. If you accumulate 500 “Yes” contracts, stop bidding for more until some are sold | All market makers |

| Inventory skew | If you’re accumulating too much on one side, shift your bid/ask quotes to discourage further fills on that side and encourage offsetting fills | Semi-automated and professional |

| Market selection | Only make markets in events with no scheduled news catalysts in the next 24 hours. Avoid the hour before and after major data releases | All market makers |

Capital Requirements and Realistic Returns

Market making requires significantly more capital than directional trading because you need to maintain inventory on both sides of the market simultaneously.

| Level | Capital | Approach | Monthly Return | Annualized |

|---|---|---|---|---|

| Learning | $1,000–$5,000 | 1–2 markets, manual order management | $50–$200 | 12–48% |

| Semi-Automated | $5,000–$25,000 | 5–10 markets, bot-assisted quoting | $200–$1,000 | 12–48% |

| Diverse Portfolio | $25,000–$100,000 | 20+ markets, fully automated | $1,000–$5,000 | 12–60% |

| Professional | $100,000+ | Cross-platform, sub-10ms latency | $5,000–$20,000+ | 24–60%+ |

(Source: NYC Servers Guide to Prediction Market Making)

⚠️ Reality check on these numbers: The upper ranges require professional-grade infrastructure (co-located servers, direct exchange connectivity, custom trading software). At the learning stage with manual order management, expect the lower end of returns — and expect some months to be negative due to adverse selection events. This is not passive income.

The Capital Lock Problem

Unlike directional trading (where your capital is released at resolution), market making locks capital continuously. You need to maintain standing orders on both sides of multiple markets, which means your capital is always deployed. Factor in the opportunity cost of this permanent deployment when evaluating returns.

Platform Considerations

Polymarket

- Best for market making due to gasless limit orders, transparent on-chain book, and API access

- CLOB architecture is compatible with standard market-making algorithms

- No explicit fees on order placement or cancellation — critical for the frequent order management that market making requires

- Risk: Decentralized resolution (UMA oracle) adds a layer of uncertainty for positions held through resolution

Kalshi

- Fully centralized CLOB with professional-grade order management

- Higher fee friction makes the minimum profitable spread wider — you need to quote wider to cover costs

- More suitable for higher-volume, institutional-grade market making

- Advantage: Regulatory protections and predefined resolution reduce the tail risk of market making through resolution

Optimal Approach

Many serious market makers operate on both platforms simultaneously, choosing Polymarket for its lower friction on high-frequency quoting and Kalshi for markets with clearer resolution criteria and more predictable institutional order flow.

Market Making vs. Directional Trading: When to Choose Which

| Factor | Market Making | Directional Trading |

|---|---|---|

| Edge required | Structural (spread capture) | Analytical or informational |

| Win rate | High (most fills are profitable) | Variable (depends on analysis quality) |

| Per-trade profit | Small (the spread) | Variable (potentially large) |

| Risk profile | Many small profits, occasional large losses (adverse selection) | Variable profits and losses |

| Capital needs | High (inventory on both sides) | Lower (single-side exposure) |

| Time commitment | High (continuous monitoring) | Variable (research-heavy, execution-light) |

| Technical requirements | API access, automation, latency management | Spreadsheets and analysis; API optional |

| Best for | Traders who are good at risk management and systems | Traders who are good at analysis and research |

Blending the two: Some traders use market making as their “base income” (steady, small profits from spread capture) and layer directional trades on top when they identify high-conviction analytical edge. The market-making infrastructure (always having orders on the book, always watching the market) naturally puts you in a good position to spot directional opportunities.

Getting Started: A Practical Path

Phase 1: Learn by Watching (Week 1–2, $0 cost)

- Choose one stable Polymarket market with moderate volume

- Open the order book and watch for a full trading day

- Note: How often do bids/asks fill? How wide is the spread? How volatile is the price?

- Paper-trade: imagine placing a bid at X and an ask at Y. Track when each would fill and calculate your theoretical P&L

Phase 2: Manual Market Making (Week 3–6, $1,000–$2,000)

- Start with ONE market. One only.

- Place a bid and ask symmetrically around the mid-price with a $0.04–$0.06 spread

- When one side fills, immediately consider: should you re-quote, widen, or hedge?

- Manually manage your inventory — sell excess “Yes” or “No” positions to rebalance

- Track every fill and calculate your daily P&L including adverse selection events

- Accept that you will make mistakes. This phase is tuition, not income

Phase 3: Semi-Automated (Month 2+, $5,000+)

- Learn the Polymarket API or Kalshi API

- Build or acquire a simple bot that automatically places, adjusts, and cancels orders based on predefined rules

- Expand to 3–5 markets

- Implement basic risk management: position limits, automatic quote widening before scheduled events

Phase 4: Scale (Month 6+, $25,000+)

By this point, you’ll have enough experience and data to decide whether market making is worth pursuing at scale. If your Phase 2–3 P&L is consistently positive after adverse selection, scale capital and market coverage. If it’s breakeven or negative, this strategy may not suit your disposition or competitive position.

What You Learned

In this module, you learned:

- Market making earns the spread by providing liquidity on both sides — it profits from volume, not prediction

- Adverse selection is the primary risk: informed traders pick off your orders before you can cancel, creating losses that exceed many spread profits

- Capital requirements start at $1,000–$5,000 for learning and scale to $100,000+ for professional operations

- Stable, high-volume markets with retail-heavy order flow are ideal; fast-moving news-driven markets are hostile

- A 4-phase progression (observe → manual → semi-automated → scaled) provides a structured learning path

What’s Next

Congratulations — you’ve completed Level 3: Strategy. 🎓

You now have a comprehensive strategic toolkit: arbitrage, data-driven analysis, bias exploitation, fundamental analysis, and market making. Level 4 brings it all together — building a trading system, advanced risk management, portfolio construction, psychology, and the superforecaster mindset.

→ Level 4: Mastery — Module 4.1: Building Your Trading System

🎯 Try This Now: Open a stable Polymarket market and study the order book for 15 minutes. Watch who fills: are the fills mostly market orders eating the ask/bid? Or limit orders matching? Count how many bid-side fills and ask-side fills occur in 15 minutes. Estimate: if you’d been providing the ask at the current best price with 100 contracts, how many fills would you have gotten? What’s the spread you’d have earned? Now ask: were there any rapid price movements during those 15 minutes where you would have been adversely selected? This observation exercise builds the intuition that no amount of theory can replace.

Predictionist School is a free educational resource from Predictionist.com. We may earn referral commissions from platforms we recommend — see our disclosure policy for details. This content is for educational purposes only and does not constitute financial advice.