4.1 Building Your Trading System

Key Takeaways

- A trading system is not software — it’s a documented, repeatable process that removes emotion from your decisions

- The system has four components: market selection, entry criteria, position sizing, and exit rules — all defined before you trade

- The Kelly Criterion provides mathematically optimal position sizing, but practical traders use Half-Kelly or Quarter-Kelly because overestimating your edge leads to catastrophic overbetting

- A 15% drawdown circuit breaker forces you to stop trading and reassess when losses accumulate — this single rule prevents most blow-ups

- Paper trading → small live → full size is the only safe validation sequence — skipping stages is the most common cause of avoidable losses

Scope: This module teaches you to integrate everything from Levels 1–3 into a personal, documented trading system. It connects directly to the strategies from Level 3 and sets up the operational infrastructure for Module 4.2: The Trading Journal.

What Is a Trading System?

A trading system is your pre-committed set of rules for how you trade. It answers four questions before you ever look at a market:

- What do I trade? (Market selection criteria)

- When do I enter? (Entry conditions)

- How much do I risk? (Position sizing)

- When do I exit? (Exit rules)

The purpose of a system is to eliminate in-the-moment emotional decisions. When you’re watching a market spike and your adrenaline is pumping, you don’t want to be deciding how much to bet. You want to be executing a pre-made decision.

Component 1: Market Selection

Not every market is worth your attention. Your system should define explicit filters:

Selection Filters

| Filter | Purpose | Example Rule |

|---|---|---|

| Category | Focus on markets where you have analytical edge | “I only trade economic indicators and Fed decisions” |

| Liquidity minimum | Avoid markets where you can’t enter/exit efficiently | “Minimum $50,000 in 24-hour volume” |

| Resolution clarity | Avoid ambiguous resolution criteria | “Resolution source must be a named government agency or wire service” |

| Time to resolution | Match your capital deployment horizon | “Resolves within 90 days” |

| Edge threshold | Only trade when the gap between your estimate and market price exceeds TFT | “My estimate must diverge from market price by ≥2× my TFT” |

The discipline: If a market doesn’t pass all five filters, you don’t trade it. No exceptions for “I just have a feeling about this one.”

Component 2: Entry Criteria

Your entry criteria define the specific conditions under which you open a position. They should be written as if-then statements:

Template

IF [market passes all selection filters] AND [my probability estimate is X] AND [the market price is Y] AND [the gap (X−Y) exceeds 2× my TFT] AND [the order book has sufficient depth for my position size] THEN enter the position.

Entry Types by Strategy

| Strategy | Entry Trigger |

|---|---|

| Data-driven | Your model output diverges from market price by ≥ edge threshold after new data release |

| Bias exploitation | Market-wide screening identifies contracts priced in the bias zone (e.g., longshots at $0.05–$0.15) with base rate divergence |

| Fundamental analysis | Your actor profile + reference class analysis produces an estimate ≥ 15 points from market price |

| Arbitrage | Scanner identifies cross-platform spread exceeding Go/No-Go checklist thresholds |

| Market making | Stable market with no scheduled catalysts in 24 hours, spread ≥ your minimum profitable width |

Component 3: Position Sizing — The Kelly Criterion

Position sizing is the most important component of your system. Get it wrong and even a genuine edge leads to ruin.

The Kelly Criterion

The Kelly Criterion calculates the mathematically optimal fraction of your bankroll to bet on a single trade:

Kelly % = (Edge / Odds)

Where:

- Edge = Your estimated probability − Market implied probability

- Odds = The payout ratio (for binary contracts at price p: odds = (1−p)/p for buys, p/(1−p) for sells)

Simplified for Prediction Markets

For a binary contract you’re buying at price p, where you estimate the true probability is q:

Kelly % = q − p / (1 − p)

Example:

- Market price (p): $0.40

- Your estimate (q): 0.55 (55%)

- Kelly % = 0.55 − 0.40 / (1 − 0.40) = 0.55 − 0.667 = …

Let’s use the clearer form:

Kelly % = (q × odds − (1−q)) / odds Where odds = (1−p) / p

- Odds = 0.60 / 0.40 = 1.5

- Kelly % = (0.55 × 1.5 − 0.45) / 1.5 = (0.825 − 0.45) / 1.5 = 0.375 / 1.5 = 25%

Kelly says bet 25% of your bankroll on this trade.

Why Full Kelly Is Dangerous

The Kelly Criterion assumes your probability estimate is perfectly accurate. It’s not. Even small errors in your estimate can lead to dramatically different optimal sizes:

| Your True Edge | Kelly Suggests | What Happens |

|---|---|---|

| Exactly as estimated | 25% | Optimal growth |

| 5% lower than estimated | 15% | Still profitable but you’ve massively overbet |

| 10% lower than estimated | 5% | Breakeven — you’ve bet 5× too much |

| Actually no edge | 0% | You’ve bet 25% of your bankroll on a coin flip |

The solution: fractional Kelly.

| Fraction | Sizing | Best For |

|---|---|---|

| Full Kelly | 25% (in our example) | Never use this in practice |

| Half Kelly | 12.5% | Experienced traders with well-validated models |

| Quarter Kelly | 6.25% | Most traders; provides significant edge capture with large protection against estimate errors |

| The 5% Rule | 5% max | The floor from Module 1.4 — never exceed this regardless of Kelly output |

Our recommendation: Use Quarter Kelly with a 5% cap. This means: calculate Quarter Kelly, and if it exceeds 5% of your bankroll, cap it at 5%. This provides an excellent balance between edge capture and survivability.

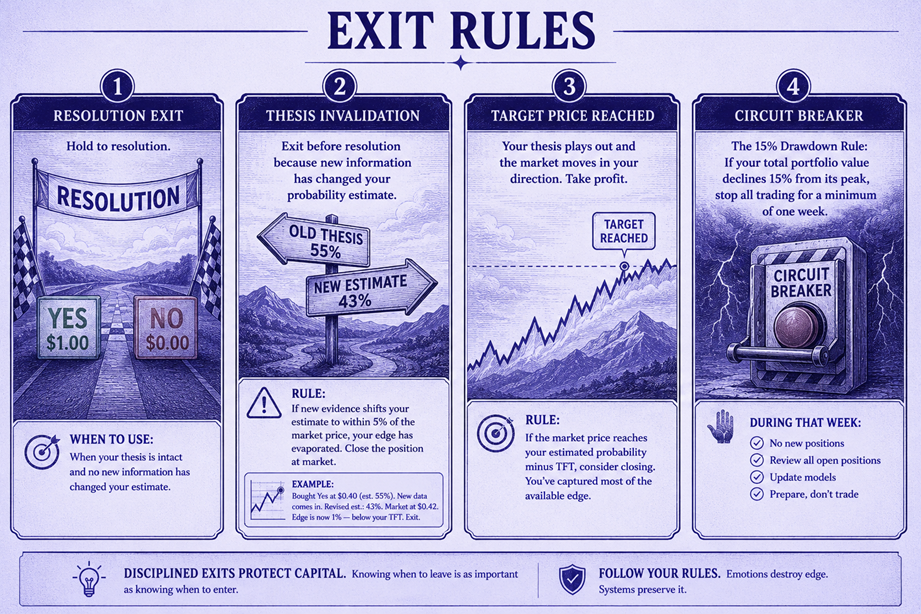

Component 4: Exit Rules

Your system must define when and how you close positions. There are four exit types:

Exit Type 1: Resolution Exit

Hold to resolution. The market resolves and pays $1.00 or $0.00. This is the default exit for most prediction market trades.

When to use: When your thesis is intact and no new information has changed your estimate.

Exit Type 2: Thesis Invalidation

Exit before resolution because new information has changed your probability estimate.

Rule: If new evidence shifts your estimate to within 5% of the market price, your edge has evaporated. Close the position at market.

Example: You bought “Yes” at $0.40 (your estimate: 55%). New data comes in. Your revised estimate: 43%. Market is at $0.42. Your edge is now only 1% — below your TFT. Exit.

Exit Type 3: Target Price Reached

Your thesis plays out and the market moves in your direction. Your original 15-point gap has narrowed to 3 points. Take profit.

Rule: If the market price reaches your estimated probability minus TFT, consider closing. You’ve captured most of the available edge.

Exit Type 4: Circuit Breaker

The 15% Drawdown Rule: If your total portfolio value declines 15% from its peak, stop all trading for a minimum of one week. During that week:

- Review every open position and every recent trade

- Determine whether the drawdown is due to bad luck (variance) or a systematic error in your approach

- If variance: resume at Half Kelly sizing for the next 20 trades before returning to normal

- If systematic error: fix the system before trading again

This rule exists because the most common failure mode in trading is not a single bad trade — it’s a series of escalating bad trades driven by the emotional need to “win back” losses.

The Paper Trading Phase

Before deploying any system with real money, paper trade it for a minimum of 4 weeks or 30 trades (whichever comes first):

Paper Trading Protocol

- Use a spreadsheet or journal — log every trade as if it were real

- Use real market prices — no “I would have gotten a better fill” retcons

- Apply all system rules — selection filters, entry criteria, position sizing, exit rules

- Track results honestly — record every win and loss; calculate aggregate P&L, win rate, and average edge

Validation Criteria

After your paper trading phase, evaluate:

| Metric | Passing | Failing |

|---|---|---|

| Aggregate P&L | Positive | Negative |

| Win rate | Consistent with strategy type (e.g., 15–25% for longshots, 50%+ for data-driven) | Significantly below expected |

| Average edge realized | Within 50% of your pre-trade estimates | Your estimates are systematically off |

| Max drawdown | <15% | Hit circuit breaker during paper trading |

| Emotional discipline | You followed the rules consistently | You overrode your system multiple times |

If all five pass: Move to live trading with 25% of your intended position sizes for the first 20 trades, then scale up. If any fail: Diagnose and fix before going live. There is no cost to extending paper trading. There is significant cost to premature live deployment.

System Templates by Strategy

Template A: Data-Driven System

SELECTION:

Economic/weather markets with clean data inputs.

Volume >$50K/day. Resolution within 60 days.

ENTRY:

Model output diverges from market price by ≥ 2× TFT.

Limit order at mid-spread.

SIZING:

Quarter Kelly, capped at 5%.

EXIT:

Hold to resolution unless thesis invalidated by new data.

Close if revised estimate within 5% of market price.

CIRCUIT:

15% portfolio drawdown → stop 1 week.

Template B: Bias Exploitation System

SELECTION:

All markets on Polymarket/Kalshi meeting liquidity minimums.

Screen for longshots ($0.05–$0.15) with base rate divergence ≥50%.

ENTRY:

Limit orders on qualifying longshots. Certainty-premium buys at $0.95–$0.97.

SIZING:

Equal-weight across 20+ positions. Max 3% per position.

EXIT:

Hold all positions to resolution.

No early exits (portfolio strategy requires full sample).

CIRCUIT:

15% portfolio drawdown → review bias identification methodology.

Template C: Arbitrage System

SELECTION:

Same event on 2+ platforms. Net spread after TFT ≥ $0.02.

Resolution criteria functionally identical.

ENTRY:

Simultaneous limit orders on both platforms.

Both legs must fill within 60 seconds or cancel both.

SIZING:

Per Go/No-Go checklist (Module 3.2). Max 10% per arb pair.

EXIT:

Hold to resolution (risk-free after both legs fill).

CIRCUIT:

If 3 consecutive arbs show slippage exceeding estimates → recalibrate friction model.

What You Learned

- A trading system has four components: market selection, entry criteria, position sizing, and exit rules — all defined before you trade

- Quarter Kelly with a 5% cap is the recommended position sizing approach — it balances edge capture with protection against estimation errors

- The 15% drawdown circuit breaker prevents cascading losses driven by emotional escalation

- Paper trading for 30+ trades before going live validates your system without risking capital

- System templates provide starting points that you customize based on your strategy, capital, and risk tolerance

What’s Next

Your system tells you what to do. The trading journal tells you whether it’s working. The next module teaches you to build the feedback loop that turns trading from guessing into iterating.

→ Module 4.2: The Trading Journal

🎯 Try This Now: Write your trading system on a single page. Use one of the templates above as a starting point and customize it for your situation. Define your five selection filters, your entry conditions, your sizing rule (Quarter Kelly with 5% cap), and your four exit types. Pin it next to your screen. This document is your trading constitution — follow it before every trade.

Predictionist School is a free educational resource from Predictionist.com. We may earn referral commissions from platforms we recommend — see our disclosure policy for details. This content is for educational purposes only and does not constitute financial advice.